Two years into the pandemic, what impacts have COVID-19 really had on university finances and staffing in 2020 and in 2021? Recently published research shows the impacts varied greatly across the sector. However, staff cuts appear to have been disproportionate to overall financial losses.

About 10% of the university workforce (in full-time equivalent terms) lost their jobs. Although that broadly matches the loss of fees and charges income in 2020, overall revenue fell by only 5%.

The impacts of the pandemic on revenue have been generally less than predicted. About half of Australia’s public universities suffered medium to high financial impacts. Eight universities increased or had essentially the same total income in 2020 as in 2019.

Looking ahead, anticipated increases in other revenue provide a healthy buffer against any further fall in international student revenue.

COVID halted a decade of growth

From 2010 to 2019, domestic student enrolments grew by 27% and overseas student enrolments by 56%. Total annual revenue from continuing operations increased by 65% to nearly A$37 billion in 2019.

As a share of revenue, government financial assistance, including student HECS payments, decreased from 56% to 49%. Revenue from fees and charges grew from 23% to 32%.

By the end of 2019, universities’ total equity was $61.5 billion. Many universities, but not all, had a strong buffer to manage the financial challenges of the pandemic.

In mid-2020, amid first-wave lockdowns and border closures, several commentators predicted the impact on international student enrolments would be worse than the actual 2020 outcome. We predicted a 2020 fee loss of up to $3.5 billion. It turned out to be $1.16 billion – a 10% reduction in fee income.

In February 2021, Universities Australia announced universities had lost $1.8 billion in revenue for 2020 and faced a $2 billion loss in 2021.

In August 2021, federal Education Minister Alan Tudge said the sector had begun the year in a relatively strong financial position, with an overall operating surplus of about 2%. He said international student enrolments had fallen by only 5% in 2020 and by 12% by mid-2021 against the record levels of 2019.

Staffing typically accounts for 57% of university spending. Universities Australia reported in February 2021 at least 17,300 university jobs had been lost. By September 2021 the Australia Institute’s Centre for Future Work calculated one in five tertiary education jobs had been lost – including 35,000 at public universities.

6 conclusions about the impacts

The outcomes in 2020 are now well documented. However, mixed messages about revenue losses in 2021 and beyond make for a confusing picture. Based on our research, we offer six conclusions.

1. The impact of the pandemic on higher education finances in 2020 was significant but not catastrophic.

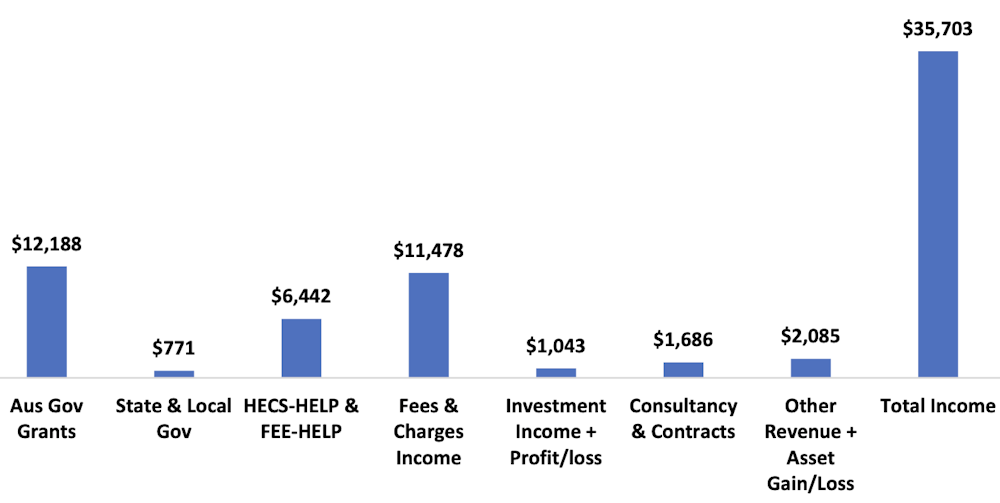

For 2020, total revenues fell by 5% or $1.82 billion to $36 billion.

Fees and charges revenue (mostly international student fees) fell by 10% or $1.2 billion.

The loss of investment revenue ($1.3 billion) in 2020 was similar.

Increased government grants and other revenue partly offset these losses.

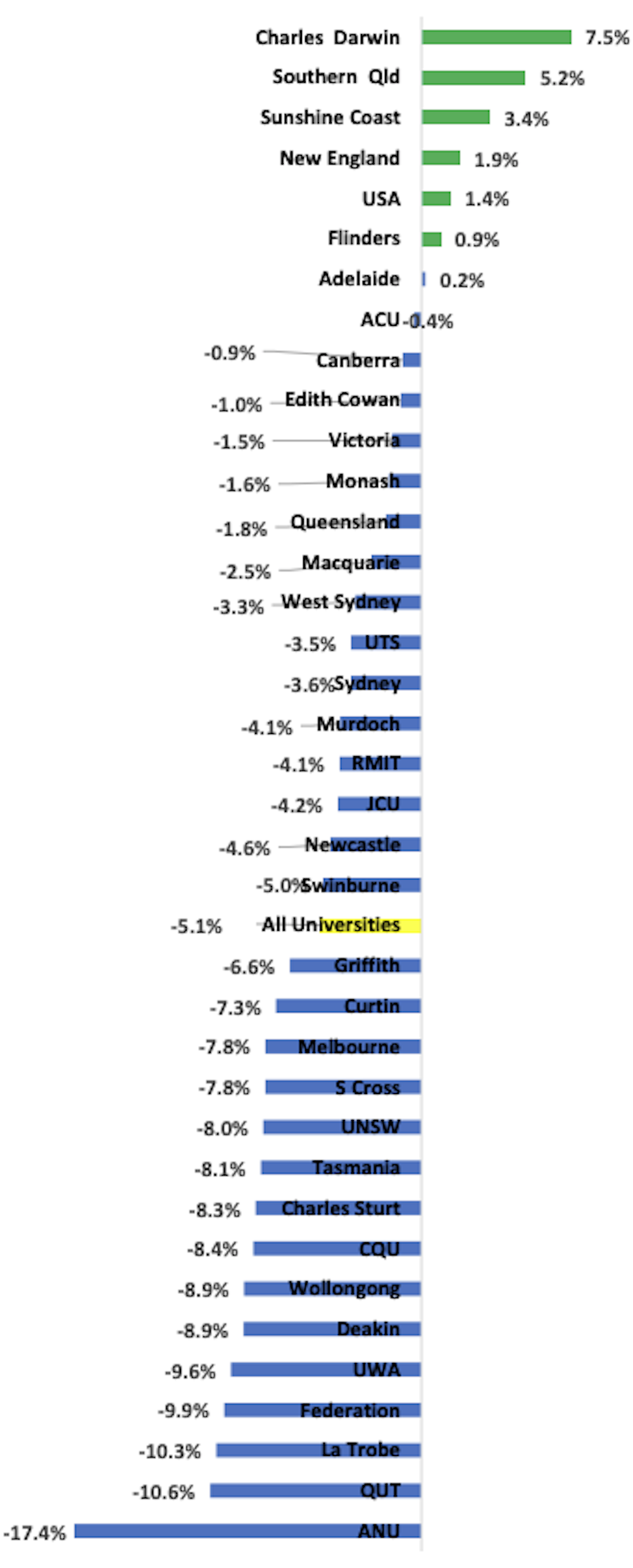

2. The impacts on individual universities were highly variable.

Eight universities increased or had essentially the same total income in 2020 as in 2019. They include the three South Australian public universities, four regional universities and ACU as a multistate university. Charles Darwin University reported a sector-high revenue increase of 7.5%.

Ten universities reported revenue losses exceeding 8%. Four were regional, two were in the Group of Eight and three were in Victoria, the state most affected by lockdowns in 2020. ANU reported a sector-high revenue loss of 17.4%.

Among the larger universities, Monash was a standout. It had only a 1.6% revenue loss and a 2.9% increase in fees and charges revenue despite lower international student enrolments.

We conclude the pandemic had a high financial impact on ten universities and a medium impact on another ten.

3. International student enrolments – and hence fees and charges revenue – appear to be declining much faster in 2021 than for 2020.

As at September 2021, the Commonwealth’s Provider Registration and International Student Management System (PRISMS) database shows:

commencing international student enrolments fell by 24% compared to 2020 and by 41% compared to 2019

for all international enrolments, numbers fell by 13% compared to 2020 and by 17% compared to 2019.

The initial 4% fall in PRISMS enrolments in 2020 corresponded to a 10% decline in total fees and charges revenue. It appears reasonable, then, to assume the 13% decline in PRISMS enrolments for 2021 might equate to a 20-30% reduction.

4. Anticipated increases in other revenue in 2021 will provide a healthy buffer against further falls in international student revenue.

University revenue from government grants, student HECS payments and other income increased by 3% in 2020. We expect the Job-Ready Graduates Package and other sources will enable universities to increase revenue from these sources by at least 5%, or $1.1 billion, in 2021.

The Commonwealth also allocated an extra $1 billion in research funding in 2021.

As financial markets have improved significantly since December 2020, investment revenue can be expected (barring another major disruption) to return at least to 2019 levels of $1.3 billion.

These three items combined represent an increase of $3.4 billion.

International fee revenue would need to fall by at least 30% in 2021 to outweigh these gains.

We conclude that 28 of 37 public universities could sustain greater fee losses in 2021 than in 2020 and still have higher total incomes.

5. If borders reopen and international students return for semester one in 2022, revenue losses will probably bottom out in 2021 and 2022.

Universities are expected to be highly flexible in enrolling international students during 2022. This suggests commencing student numbers will progressively offset the numbers who have completed courses.

Any additional losses in fees and charges revenue in 2022 are likely to be modest and offset by revenue from increasing domestic enrolments.

Responses to new COVID-19 variants remain a significant risk in assessing likely revenue impacts.

The outlooks for individual universities vary greatly. In part, these depend on pandemic impacts on international student markets across various countries. It is unlikely there will be a standard pattern of re-engagement.

6. The impact on staffing levels appears to have been disproportionate, with workers employed on casual and fixed-term contracts the worst affected.

Before the pandemic, the number of university employees totalled 137,575 full-time equivalent (FTE) positions. In FTE terms, some 95,500 were full-time staff, 17,205 fractional full-time and 24,873 casual.

We extrapolated the numbers of jobs lost by December 2020 based on annual reporting by the seven Victorian universities (the only ones to provide such data). These data suggest 20,000 jobs (equating to 7,000 FTE) had been lost across the sector by the end of 2020.

The Centre for Future Work, using ABS data, later calculated public university job losses had risen to 35,000. Extrapolating the Victorian data, this would amount to around 14,000 FTE positions or 10% of the workforce on a FTE basis. The difference between positions lost and the full-time equivalent number suggests casual, fixed-term and part-time staff suffered the greatest impact.

Given recent announcements of further job losses, these estimates may be conservative.

A loss of 10% of the FTE workforce broadly matches the loss of fees and charges income in 2020, though overall revenue fell by only 5%. If university finances do bottom out in 2021, the overall impact of the pandemic has amounted to a fall in annual revenues of around 5%. In this case, university staff appear to have contributed disproportionately to bridging the gap between revenue and expenditure.

It also suggests that, should revenues and the international student market rebuild, either universities will face significant workforce recruitment challenges or they entered the pandemic with significantly oversized workforces.![]()

AUTHORS: Ian Marshman, Honorary Principal Fellow, Melbourne Centre for the Study of Higher Education, The University of Melbourne and Frank Larkins, Professor Emeritus and Former Deputy Vice Chancellor, The University of Melbourne

This article is republished from The Conversation under a Creative Commons license. Read the original article.